But if multiple people handle your business’s finances, the person reconciling the accounts should probably be different from the person signing the checks. A bank may charge an account maintenance fee, typically withdrawn and processed automatically from the bank account. When preparing a bank reconciliation statement, a journal entry is prepared to account for fees deducted.

6 Define the Purpose of a Bank Reconciliation, and Prepare a Bank Reconciliation and Its Associated Journal Entries

A liability account on the books of a company receiving cash in advance of delivering goods or services to the customer. The entry on the books of the company at the time the money is received in advance is a debit to Cash and a credit to Customer Deposits. Bank Example 2 showed that the bank debits the depositor’s checking account to decrease the checking account balance (since this is part of the bank’s liability Customers’ Deposits). Bank Example 1 showed that the bank credits the depositor’s checking account to increase the depositor’s checking account balance (since this is part of the bank’s liability Customers’ Deposits). When a company writes a check, the company’s general ledger Cash account is credited (and another account is debited) using the date of the check.

- The more frequently you do a bank reconciliation, the easier it is to catch any errors.

- Know Your Business (KYB) is a set of verification procedures that helps companies avoid getting into business with criminals.

- Check that your financial transaction records include all payments and deposits for the transaction period, as well as the final balance.

- A liability account on the books of a company receiving cash in advance of delivering goods or services to the customer.

- For the past 52 years, Harold Averkamp (CPA, MBA) hasworked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online.

Compare the Deposits

Kevin has been writing and creating personal finance and travel content for over six years. He is the founder of the award-winning blog, Family Money bookkeeping and accounting task checklist Adventure, and host of the Family Money Adventure Show podcast. He has been quoted by publications like Readers Digest and The Wall Street Journal.

Step 4: Account for interest and fees

Adjust the cash balances in the business account by adding interest or deducting monthly charges and overdraft fees. Make sure that you’ve also taken into account all deposits and withdrawals to an account when preparing the bank reconciliation statement. Journal entries, also known as the original book of entries, refer to the process of recording transactions as debits and credits, and once these are recorded, the general ledger is prepared. Such errors are committed while recording the transactions in the cash book, so the balance as per the cash book will differ from the passbook.

Ask Any Financial Question

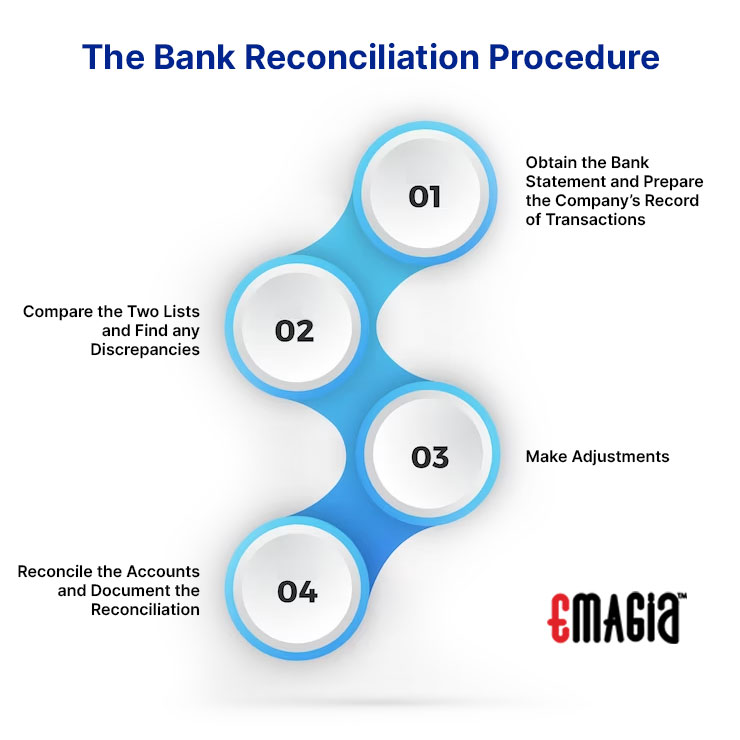

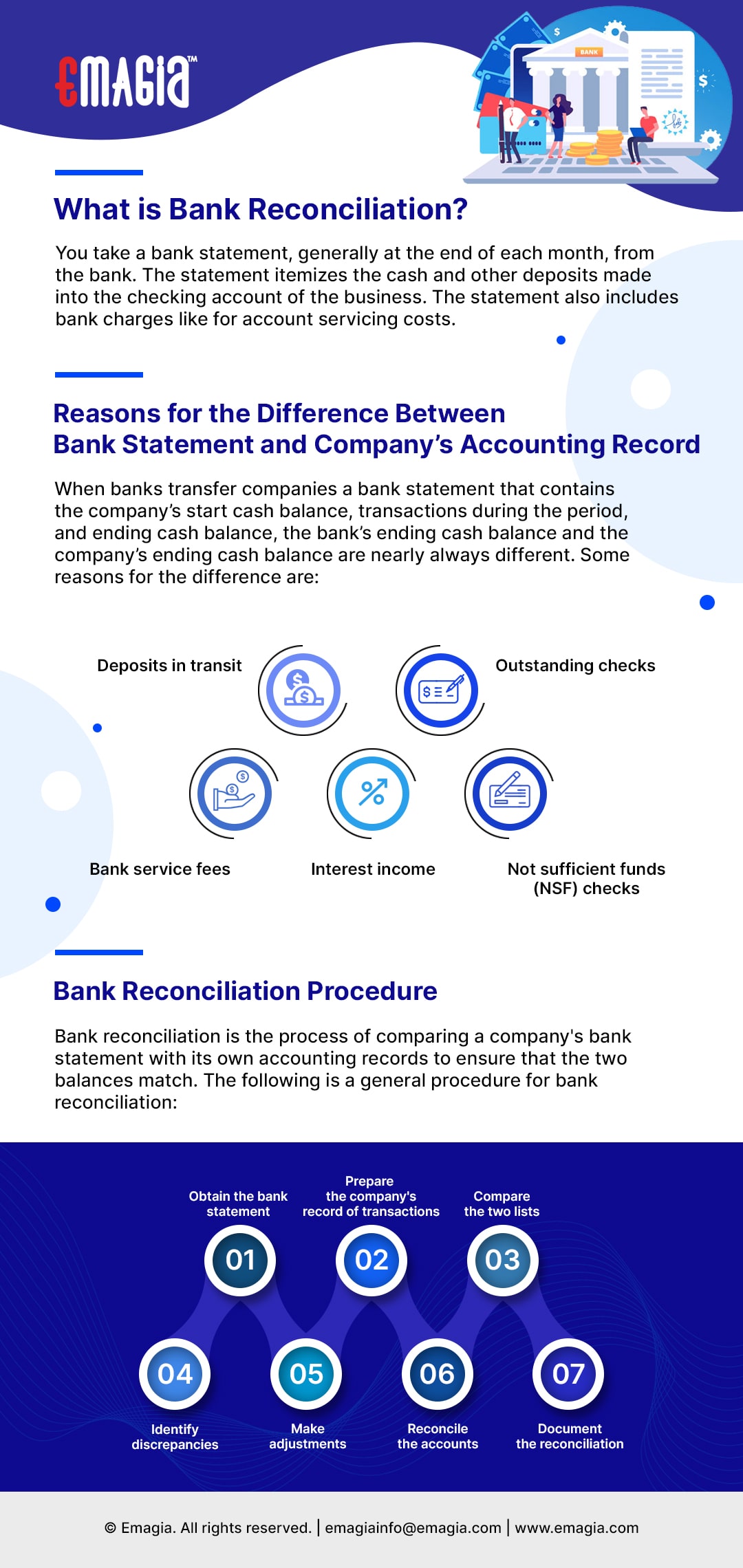

The bank reconciliation also provides a way to detect potential errors in the bank’s records. Once all differences have been identified and adjusted, it is necessary to reconcile cash balance shown on the internal records with those on the bank statement by summarizing all transactions that occurred during the period. Completing the necessary data entry duties will ensure that your accounts are accurately balanced. Then, go to the company’s ending cash balance and deduct from it any bank service fees, NSF checks and penalties, and add to it any interest earned. At the end of this process, the adjusted bank balance should equal the company’s ending adjusted cash balance.

In this step, you will compare your cash book, cash accounts, cash balances, and internal accounting records with those on the bank statement. Look for any differences in amounts, dates, or outstanding cheques that have been written but may not yet appear on the bank’s statement. Deposits in transit, for example, could be the cause of discrepancy between the bank statement balance and your internal cash position. The first step in performing a bank reconciliation is to review your bank statements for any discrepancies or unidentified transactions. This includes reviewing all deposits, withdrawals, fees, and other bank charges made that impact the final bank balance shown at the end of the month.

As a result, Community Bank’s balance sheet will report an additional $10,000 in assets and an additional $10,000 in liabilities. Accounting errors can impact your cash flow, customer service, and, ultimately, your bottom line. Bank reconciliation is an integral part of the (insert term) to ensure accuracy across your financial statements. The bank statement submitted by the businessman at the end of May will not contain an entry for the check, whereas the cash book will have the entry. Additionally, bank reconciliation statements brings into focus errors and irregularities while dealing with the cash.

These time delays are responsible for the differences that arise in your cash book balance and your passbook balance. Infrequent reconciliations make it difficult to address problems with fraud or errors when they first arise, as the needed information may not be readily available. Also, when transactions aren’t recorded promptly and bank fees and charges are applied, it can cause mismatches in the company’s accounting records. Bank reconciliation statements compare transactions from financial records with those on a bank statement. Where there are discrepancies, companies can identify and correct the source of errors.

A reconciliation of this type would be prepared for each bank account and the cash records for that account. The items in the bank section show that the bank’s version does not agree with the books because a deposit had not been processed and the checks had not yet been canceled. The bank section lists items in transit from the depositor to the bank and bank errors. The book section lists items in transit from the bank, service charges, and depositor errors. They often appear as a reconciling item because banks notify customers of the amount only through the bank statement. Errors can occur in both the recordkeeping systems of both the bank and the depositor.

The items therein should be compared to the new bank statement to check if these have since been cleared. Examples include deposited checks returned for non-sufficient funds (NSF) or notes collected on the depositor’s behalf. If you find any bank adjustments, record them in your personal records and adjust the balance accordingly.

It shows what transactions have cleared on your statement with the corresponding transaction listed in your journal. Note that this balance is different from the company’s general ledger’s Cash account balance of $7,000. Generally, neither balance is the correct amount of cash that should be reported on the company’s balance sheet. Outstanding checks are those that have been written and recorded in the financial records of the business but have not yet cleared the bank account. This often happens when the checks are written in the last few days of the month. In order to prepare a bank reconciliation statement, you’ll need to obtain both the current and the previous month’s bank statements as well as the cash book.